The Capital™

Stack System

The No Bollocks™ Framework for Funding Your Business at Every Stage

By Matt Haycox — Over £250 million raised for his own companies, over £1 billion deployed into UK SMEs, and invested in over 100 global businesses. Borrower and lender. Founder and investor. This is the complete capital playbook.

How to Use This Framework

Every business needs capital. But not every business needs the same type of capital. And not every stage of growth calls for the same funding strategy. The entrepreneur who raises venture capital for a business that should be bootstrapped is making a mistake just as costly as the entrepreneur who bootstraps a business that needs venture capital. The difference between the two is not ambition or intelligence — it is understanding.

The Capital Stack System™ is a framework for understanding every type of capital available to you, when each type is appropriate, how to access it, and — critically — the hidden costs and trade-offs that nobody tells you about until it is too late. It is called a "stack" because the most successful businesses do not rely on a single source of funding. They layer multiple types of capital on top of each other, each serving a specific purpose, each appropriate for a specific stage of growth.

I have raised over £250 million for my own companies, deployed over £1 billion into UK SMEs and invested in over 100 global businesses. I have been the borrower and the lender. The founder and the investor. The person writing the cheque and the person cashing it. This framework is the distillation of everything I have learned from sitting on every side of the table.

It is structured as five layers, from the bottom of the stack (lowest risk, lowest cost, most control) to the top (highest risk, highest cost, least control). Each layer builds on the one below it. Your job is to understand all five, identify where your business sits today, and build a capital strategy that matches your stage, your ambition, and your risk tolerance.

Why Most Entrepreneurs Get Funding Wrong

The funding landscape is a minefield, and most entrepreneurs walk through it blindfolded. They make one of four critical mistakes:

Mistake 1: They Raise Too Early

They seek external capital before they have proven that the business model works. This means they give away equity at the lowest possible valuation, diluting themselves unnecessarily. Worse, it means they are spending someone else's money to figure out whether the business is viable — which is an expensive way to learn.

Mistake 2: They Raise the Wrong Type

They take equity investment when they should be using debt. They use personal savings when they should be using grants. They take on high-interest debt when they qualify for government-backed loans. Every type of capital has a cost, and using the wrong type means paying more than you need to — in money, in equity, or in control.

Mistake 3: They Raise Too Much

Counterintuitive, but true. Raising more money than you need creates a false sense of security. It encourages overspending, premature hiring, and a lack of discipline. The best-funded startups in history have also produced some of the most spectacular failures, precisely because too much capital masked fundamental problems in the business model.

Mistake 4: They Don't Understand the Terms

They sign documents they do not fully understand, agree to covenants they cannot meet, and accept dilution they did not anticipate. By the time they realise what they have agreed to, it is too late to renegotiate.

The Capital Stack System™ eliminates these mistakes by giving you a complete map of the funding landscape and a clear framework for navigating it.

The Five Layers: An Overview

The stack is designed to be climbed from the bottom up. Each layer validates the business for the layer above it. A business that has been successfully bootstrapped is more attractive to grant bodies. A business with grant funding is more attractive to lenders. A business with debt capacity is more attractive to angel investors. Skipping layers is possible but risky — and usually expensive.

Bottom = Cheapest & Most Control → Top = Most Expensive & Least Control

| Layer | Name | What It Is | Cost of Capital | Control Retained | Best For |

|---|---|---|---|---|---|

| 1 | Bootstrapping | Self-funding from personal resources and revenue | Zero financial cost (but high opportunity cost) | 100% | Validating the idea, proving the model |

| 2 | Grants & Government | Non-repayable funding from public sources | Zero financial cost (but high time cost) | 100% | R&D, innovation, social impact ventures |

| 3 | Debt | Borrowed money that must be repaid with interest | Interest payments (5-25% APR) | 100% (if covenants are met) | Scaling a proven model, bridging cash flow gaps |

| 4 | Angel & Seed | Equity investment from individuals and small funds | Equity dilution (10-25%) | Shared (board seat, reporting) | First external capital, pre-revenue or early revenue |

| 5 | Institutional | Equity investment from VC funds, PE firms, and strategic investors | Significant equity dilution (15-40%+) | Significantly shared (board control, governance) | Rapid scaling, market expansion, pre-exit growth |

BOOTSTRAPPING

"Self-funding, revenue-funding, and the art of building with nothing."

What This Layer Is About

Bootstrapping is the foundation of the entire capital stack. It is the process of building a business using only your own resources — personal savings, revenue from early customers, and sheer resourcefulness. It is the hardest way to build a business, and it is also the most valuable, because it forces you to develop the discipline, creativity, and financial rigour that will serve you at every subsequent stage.

Every business should start here. Even if you plan to raise millions in venture capital eventually, the period of bootstrapping is where you prove that the business model works, that customers will pay, and that you can execute. Without this proof, everything else is speculation.

The Economics of Bootstrapping

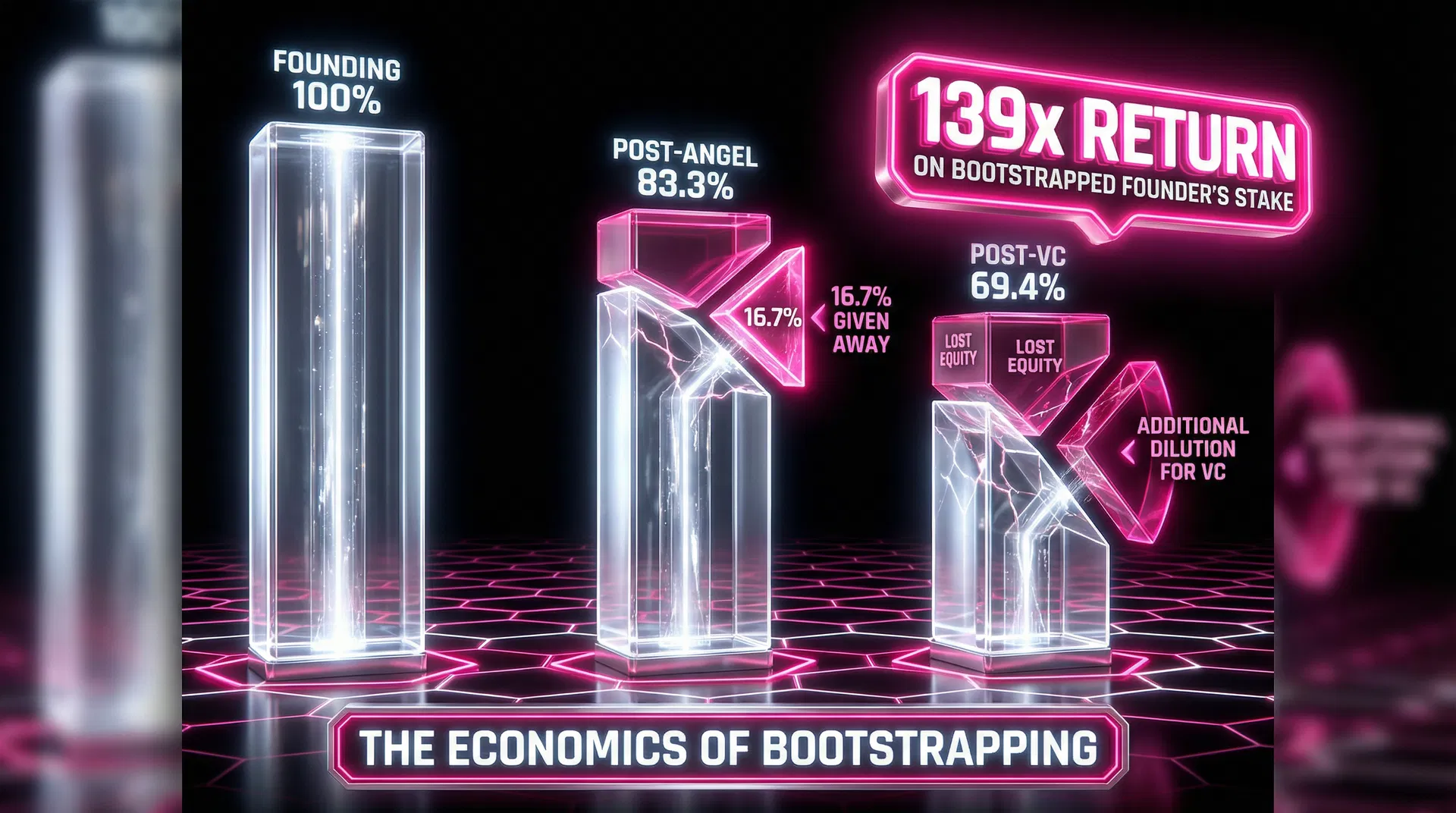

The financial logic of bootstrapping is simple but powerful: every pound you invest in the business at the earliest stage is worth dramatically more than every pound an investor puts in later, because you are investing at the lowest possible valuation.

| Scenario | Your Investment | Valuation at Investment | Your Ownership |

|---|---|---|---|

| You invest £50,000 at founding | £50,000 | £50,000 (you own 100%) | 100% |

| An angel invests £200,000 at a £1M pre-money valuation | £0 | £1,000,000 | 83.3% |

| A VC invests £2M at a £8M pre-money valuation | £0 | £8,000,000 | 69.4% |

In this scenario, your initial £50,000 investment bought you 100% of a company that is now worth £10M (post-VC money). Your £50,000 is now worth £6.94M. That is a 139x return on your personal investment. If you had not waited and let the angel invest at founding instead, your ownership would be dramatically lower, and your personal return would be a fraction of this. This is why bootstrapping matters. It is not about being cheap. It is about being strategic.

How founder ownership compounds — every percentage point retained at the start is worth dramatically more at exit

The Bootstrapping Playbook

Rule 1: Revenue Is the Best Capital

The single best source of funding for any business is revenue from customers. It is non-dilutive (you do not give up equity), non-repayable (you do not owe it back), and self-validating (if customers are paying, the business model works). Every bootstrapped business should be obsessed with generating revenue as quickly as possible.

How to Generate Revenue Before the Product Is "Ready"

| Strategy | How It Works | Example |

|---|---|---|

| Pre-sales | Sell the product before it is built. Use the revenue to fund development. | A course creator sells access to a course before recording it, using the sales to validate demand and fund production. |

| Consulting-first | Deliver the solution manually as a service before building the technology. | A SaaS founder provides the same outcome through manual consulting, then uses the revenue and insights to build the software. |

| Minimum viable product (MVP) | Build the simplest possible version that delivers the core value, and sell it. | A marketplace founder creates a simple spreadsheet-based matching service before building the platform. |

| Pilot programmes | Offer a discounted "beta" version to early customers in exchange for feedback and testimonials. | A B2B startup offers 3 months of service at 50% off to 5 pilot customers, using their feedback to refine the product. |

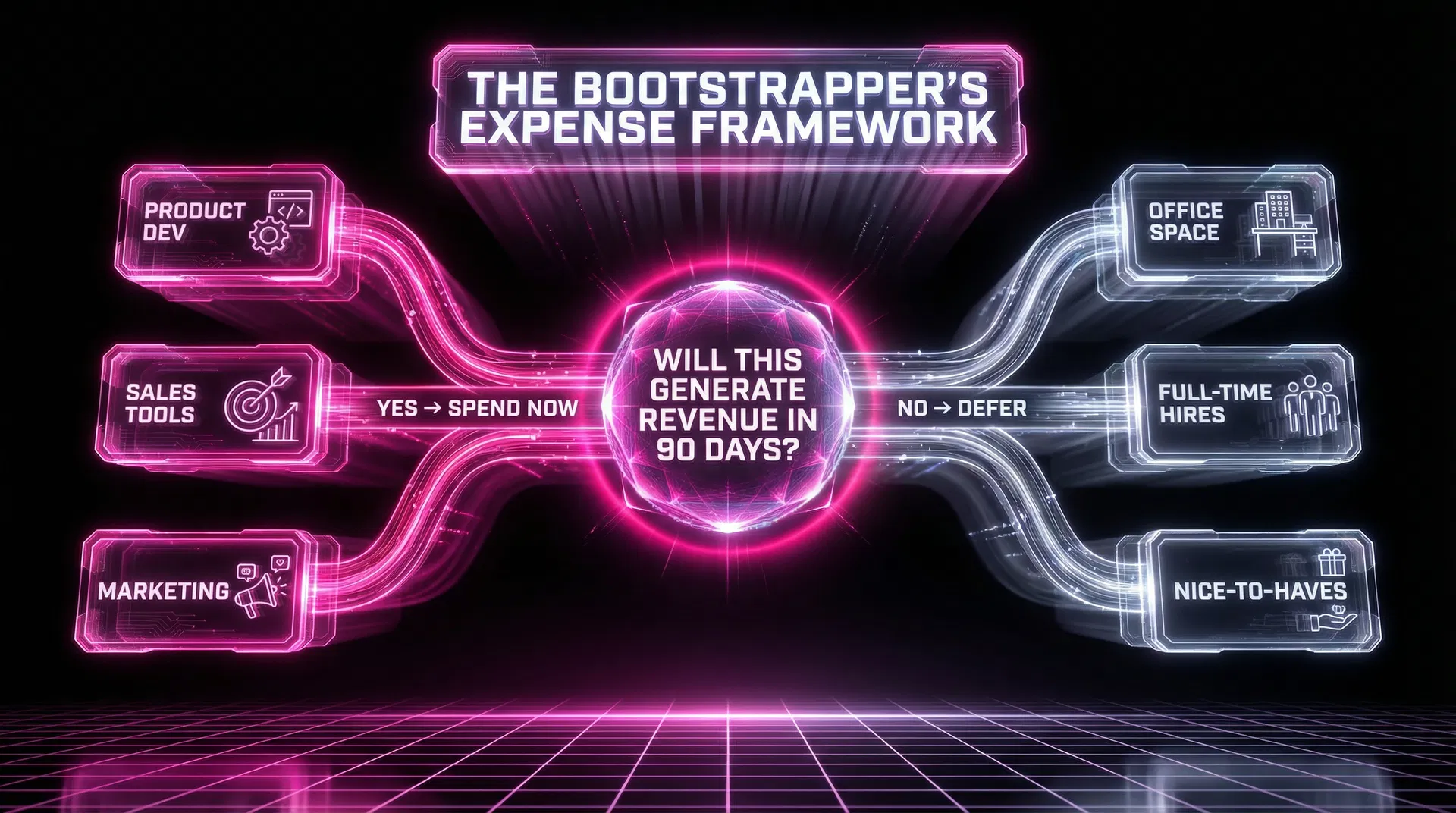

Rule 2: Control Your Burn Rate Ruthlessly

Every pound you spend during the bootstrapping phase is a pound you cannot invest in growth. This does not mean being miserly — it means being intentional. Every expense should pass the "revenue test": will this expense directly contribute to generating revenue within the next 90 days? If not, defer it.

The Bootstrapper's Expense Framework

| Expense Category | Spend Now | Defer Until Revenue |

|---|---|---|

| Product development (core features only) | ✓ | |

| Sales and customer acquisition | ✓ | |

| Office space | ✓ — work from home or a co-working space | |

| Full-time hires | ✓ — use contractors and freelancers | |

| Branding and design | ✓ — use templates and DIY tools | |

| Legal (incorporation, basic contracts) | ✓ | |

| Legal (complex IP, international structure) | ✓ | |

| Marketing (paid advertising) | ✓ — use organic channels first | |

| Technology infrastructure (enterprise-grade) | ✓ — use free tiers and open-source tools |

Every expense should pass the revenue test before you commit

Rule 3: Extend Your Runway Through Creative Financing

Bootstrapping does not mean you cannot use any external resources. It means you do not give up equity or take on significant debt. There are several ways to extend your runway without compromising ownership:

| Strategy | How It Works | Typical Value |

|---|---|---|

| Customer prepayments | Offer a discount for annual payment upfront instead of monthly | 1-12 months of cash flow acceleration |

| Supplier credit | Negotiate 30-60-90 day payment terms with suppliers | Frees up cash for other uses |

| Bartering | Exchange your services for services you need (e.g., marketing for accounting) | Variable, but can save thousands |

| Competition prizes | Enter startup competitions that offer cash prizes or in-kind support | £1,000-£100,000+ |

| Accelerator programmes | Join programmes that provide mentorship, resources, and sometimes small amounts of capital | £10,000-£150,000 plus mentorship |

When to Stop Bootstrapping

Bootstrapping is not a permanent strategy. It is a phase. You should consider moving to the next layer of the capital stack when:

| Signal | What It Means |

|---|---|

| You have proven product-market fit | Customers are paying, retention is strong, and demand exceeds your capacity to serve it |

| Growth is constrained by capital, not by demand | You have more opportunities than you can fund from revenue |

| The competitive window is closing | A well-funded competitor is gaining ground, and you need to scale faster to maintain your position |

| Unit economics are proven and positive | You know that every pound invested in growth will generate a predictable return |

Checklist — Complete Before Moving On

Have you generated revenue from at least 5 paying customers?

Do you know your unit economics (CAC, LTV, gross margin)?

Is your monthly burn rate below £5,000 (or as low as possible)?

Have you exhausted all non-dilutive funding options (prepayments, credit, bartering)?

Is growth constrained by capital rather than demand or product quality?

Can you articulate exactly what additional capital would be used for?

Every business should start here. Bootstrapping is not about being cheap — it is about being strategic.

GRANTS & GOVERNMENT

"Free money — if you know where to find it and how to get it."

What This Layer Is About

Grants are the most overlooked layer of the capital stack. Most entrepreneurs either do not know they exist, assume they do not qualify, or dismiss them as too bureaucratic to be worth the effort. All three assumptions are wrong. Government grants, innovation funding, and public-sector programmes represent billions of pounds of non-repayable, non-dilutive capital that is actively looking for businesses to fund. You do not give up equity. You do not pay interest. You do not repay the money. It is, in the most literal sense, free capital.

The catch — and there is always a catch — is that grants are competitive, slow, and heavily bureaucratic. The application process can take months. The reporting requirements can be onerous. And the criteria are often narrow, meaning your business must fit a specific profile to qualify. But for businesses that do qualify, grants can provide tens or hundreds of thousands of pounds of funding that preserves ownership and accelerates growth.

The Grant Landscape

The UK has one of the most extensive grant ecosystems in the world. Here are the major categories:

| Grant Type | Typical Amount | Who Qualifies | Key Programmes |

|---|---|---|---|

| Innovation grants | £25,000-£10M+ | Businesses developing new products, services, or processes with a technological or scientific component | Innovate UK Smart Grants, UKRI funding, Horizon Europe |

| Start-up grants | £500-£25,000 | New businesses in the first 1-3 years of trading | Start Up Loans (technically a loan at 6%), New Enterprise Allowance, Prince's Trust |

| Regional development grants | £5,000-£500,000 | Businesses located in or relocating to specific regions, often areas targeted for economic regeneration | Local Enterprise Partnership (LEP) funds, Levelling Up Fund, regional growth hubs |

| Export grants | £1,000-£50,000 | Businesses looking to sell products or services internationally | UK Export Finance, International Trade Advisors, trade mission funding |

| R&D tax credits | Up to 33% of qualifying R&D expenditure | Any UK company investing in research and development | HMRC R&D Tax Relief (SME scheme and RDEC) |

| Sector-specific grants | Variable | Businesses in targeted sectors: clean energy, life sciences, advanced manufacturing, creative industries, agritech | Sector-specific Innovate UK competitions, BEIS programmes |

| Social enterprise grants | £5,000-£250,000 | Businesses with a social or environmental mission | Big Lottery Fund, Social Enterprise Investment Fund, UnLtd |

The UK grants ecosystem — seven major categories of non-dilutive funding available to businesses

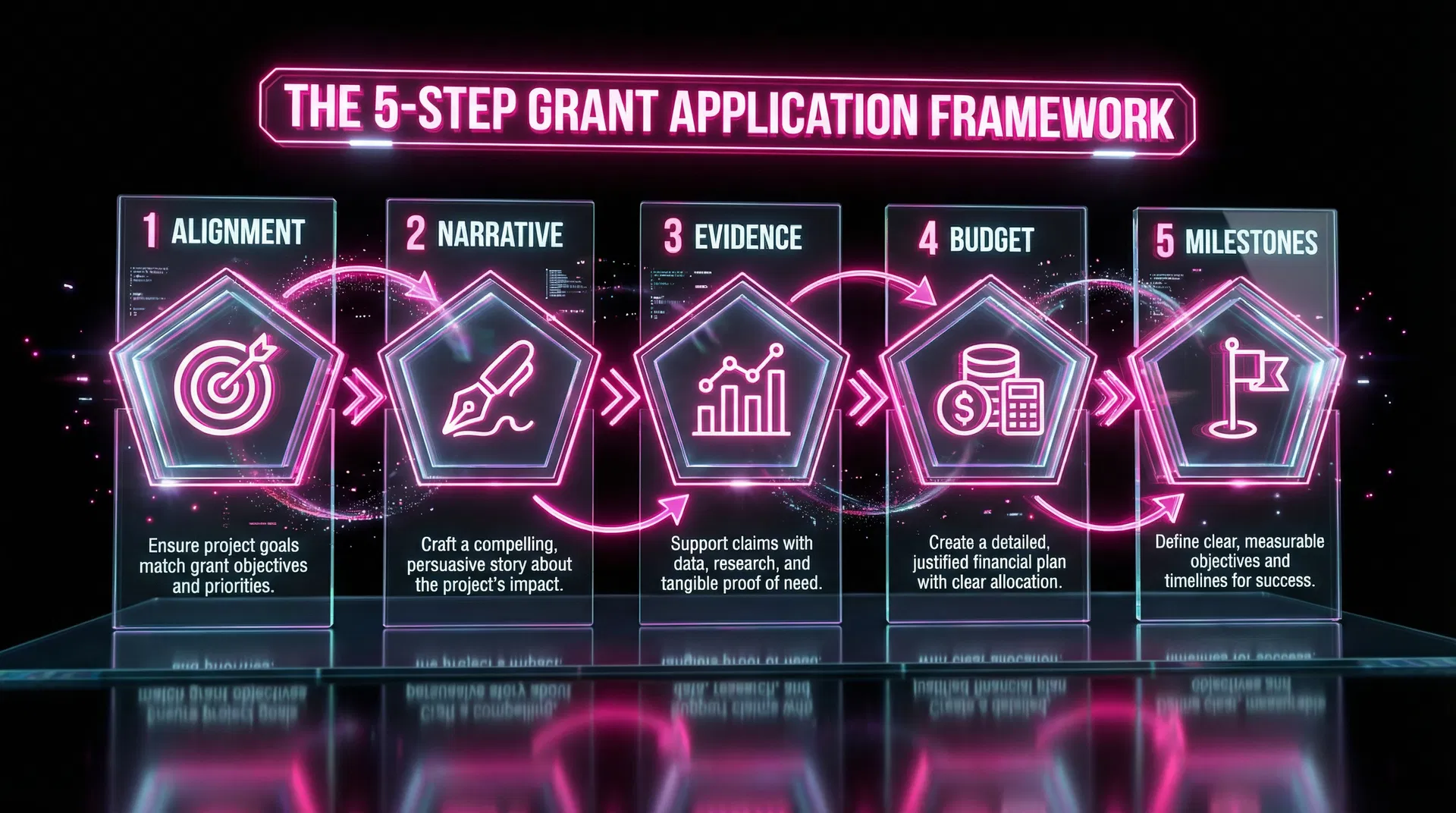

How to Win Grants

Grant applications are a skill. The businesses that consistently win grants are not necessarily the best businesses — they are the ones that understand what the grant body is looking for and present their application accordingly.

Step 1: Alignment

Before you write a single word, ensure that your project genuinely aligns with the grant's objectives. Grant bodies have specific goals — creating jobs in a region, advancing a technology, solving a social problem. Your application must demonstrate that funding your business directly advances their goals. If the fit is not genuine, do not apply. You will waste your time and damage your credibility for future applications.

Step 2: The Problem-Solution Narrative

Grant applications follow the same storytelling structure as investor pitches: problem, solution, impact. But with grants, the emphasis is on impact — specifically, the impact on the grant body's stated objectives. If the grant is designed to create jobs in the North East, your application should lead with the jobs you will create, not the revenue you will generate.

Step 3: Evidence and Credibility

Grant bodies are risk-averse. They are spending public money and must justify every allocation. Your application must demonstrate that you have the team, the track record, and the plan to deliver what you promise. Include CVs, case studies, letters of support from partners or customers, and any third-party validation of your technology or approach.

Step 4: Budget and Value for Money

Every grant application requires a detailed budget. The budget must be realistic, justified, and demonstrate value for money. Grant bodies will scrutinise every line item. Do not pad the budget — it will be caught and your application will be rejected.

Step 5: Milestones and Reporting

Grant bodies want to see a clear plan with specific milestones and deliverables. They also want to know how you will measure success. Include a Gantt chart or timeline, specific KPIs, and a reporting schedule.

Start at least 6 weeks before the deadline — grant applications are a skill that rewards preparation

Common Reasons Grant Applications Fail

| Reason | How to Avoid It |

|---|---|

| Poor alignment with the grant's objectives | Read the guidance documents thoroughly. If in doubt, call the grant body and ask. |

| Weak evidence of team capability | Include detailed CVs, relevant experience, and third-party endorsements. |

| Unrealistic budget | Base every line item on quotes, benchmarks, or historical data. |

| Vague milestones | Use specific, measurable, time-bound deliverables. |

| Poor writing quality | Have the application reviewed by someone with grant-writing experience. |

| Missing the deadline | Start the application at least 6 weeks before the deadline. |

R&D Tax Credits: The Hidden Grant

R&D tax credits deserve special attention because they are available to almost every business that is developing something new, and most businesses that qualify do not claim them. The UK government allows businesses to claim back up to 33% of their qualifying R&D expenditure — which includes staff costs, software, materials, and subcontractor costs related to research and development activities.

The definition is broader than most people think. You do not need to be building a rocket or curing a disease. If your business is seeking to advance knowledge or capability in science or technology, and the work involves overcoming scientific or technological uncertainty, it qualifies.

| Activity | Qualifies? | Why |

|---|---|---|

| Developing a new software product | Yes | Overcoming technological uncertainty in design and implementation |

| Improving an existing manufacturing process | Yes | Seeking to advance capability beyond current industry knowledge |

| Adapting an off-the-shelf product for a new use | Maybe | Only if the adaptation involves genuine technological uncertainty |

| Routine software development (e.g., building a standard website) | No | No technological uncertainty — the methods are well-established |

| Market research | No | Not a scientific or technological activity |

How to Claim: Work with a specialist R&D tax credit advisor. They will identify qualifying expenditure, prepare the technical narrative, and submit the claim to HMRC. The advisor typically charges a percentage of the successful claim (15-25%), meaning there is no upfront cost. If you have not been claiming R&D tax credits and your business does any form of development work, you are leaving money on the table.

Checklist — Complete Before Moving On

Have you searched for grants relevant to your sector, stage, and geography?

Have you identified at least 3 grants you may qualify for?

Have you read the full guidance documents for each?

Does your project genuinely align with the grant's objectives?

Have you prepared a detailed, justified budget?

Have you gathered evidence of team capability and project credibility?

Are you claiming R&D tax credits? If not, have you engaged an advisor?

Have you started the application at least 6 weeks before the deadline?

Grants are the most overlooked layer of the capital stack. Most entrepreneurs don't know they exist.

DEBT

"Borrowed capital — the most misunderstood tool in the stack."

What This Layer Is About

Debt is the most powerful and most misunderstood layer of the capital stack. Most entrepreneurs either fear it irrationally (because they associate all debt with risk) or use it recklessly (because they treat it as free money). Neither approach is correct. Debt, used properly, is the cheapest and most efficient form of growth capital available — because it does not dilute your ownership.

The logic is simple: if you can borrow money at 10% interest and deploy it in a business that generates 30% returns, you are creating 20% of value for every pound borrowed — and you keep 100% of the upside. This is the fundamental principle of leverage, and it is how the most successful businesses in the world are built.

But debt is also unforgiving. Unlike equity investors, lenders do not share in your downside. If the business fails, the debt must still be repaid. Miss a payment, and the consequences are immediate — penalties, covenant breaches, and potentially the loss of assets you pledged as security. Debt amplifies outcomes in both directions: it makes good businesses better and bad businesses worse.

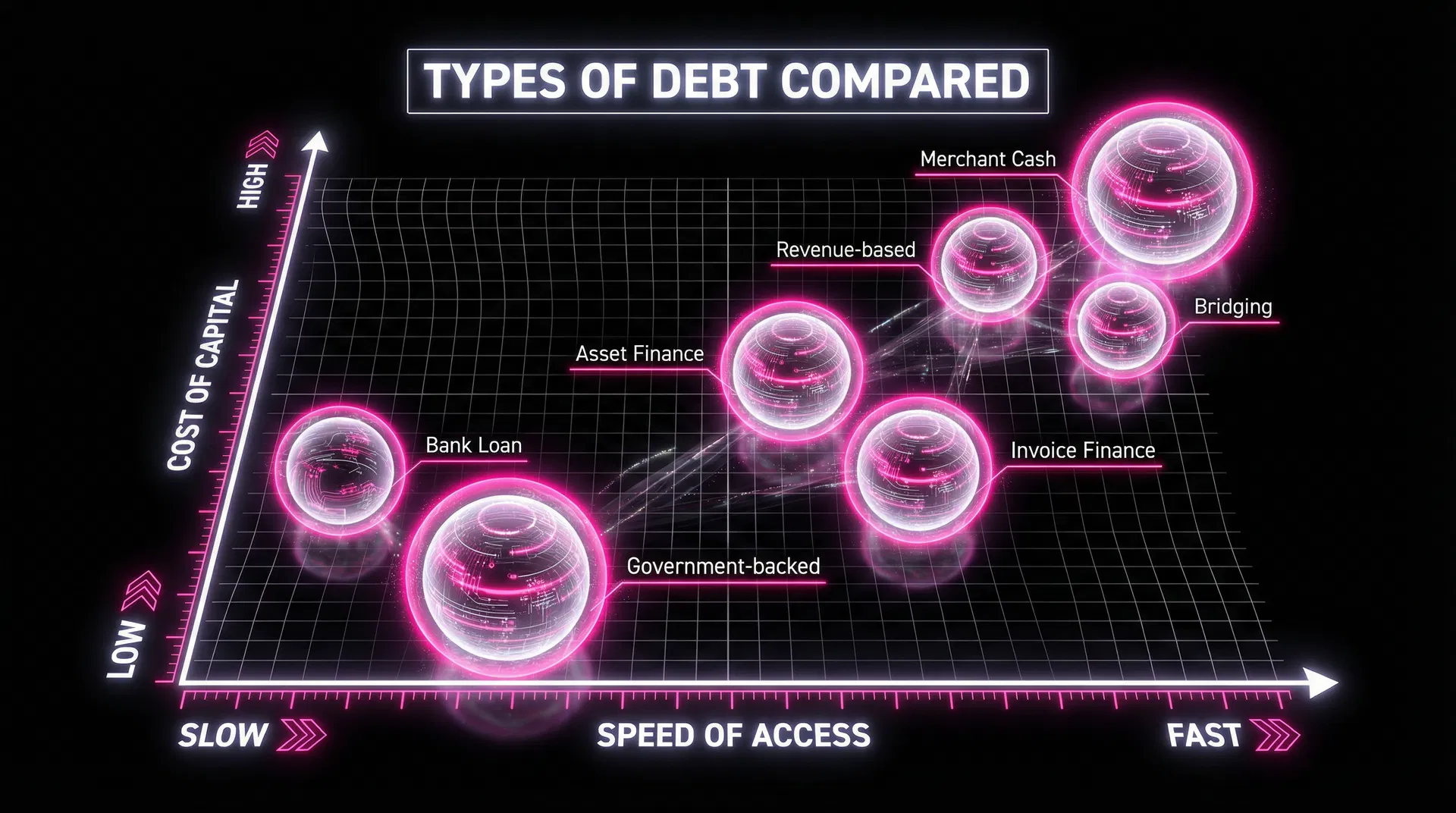

The Debt Landscape

Not all debt is created equal. The type of debt you use should match the purpose it serves and the stage of your business.

| Debt Type | Interest Rate | Security Required | Best For | Repayment Structure |

|---|---|---|---|---|

| Bank overdraft | 5-15% | Personal guarantee or business assets | Short-term cash flow smoothing | Revolving (pay interest on what you use) |

| Term loan (bank) | 5-12% | Business assets, sometimes personal guarantee | Purchasing equipment, funding specific projects | Fixed monthly payments over 1-5 years |

| Government-backed loan | 6-8% | Usually unsecured or lightly secured | Early-stage businesses that cannot access commercial lending | Fixed monthly payments over 1-5 years |

| Invoice financing / factoring | 10-25% (effective) | The invoices themselves | Businesses with long payment terms from creditworthy customers | Repaid when the customer pays the invoice |

| Revenue-based financing (RBF) | 12-30% (effective) | No security — repayment is a % of revenue | Businesses with predictable, recurring revenue | Variable — a fixed % of monthly revenue until repaid |

| Asset finance / leasing | 5-15% | The asset being financed | Purchasing vehicles, equipment, or machinery | Fixed monthly payments over the asset's useful life |

| Merchant cash advance | 20-50% (effective) | Future card sales | Retail or hospitality businesses with high card transaction volumes | Automatic deduction from daily card sales |

| Mezzanine debt | 15-25% | Subordinated to senior debt, sometimes with equity warrants | Later-stage businesses that need capital between debt and equity | Interest payments with bullet repayment at maturity |

| Convertible notes | 5-10% + conversion discount | Converts to equity at next funding round | Bridge financing between equity rounds | Converts to equity (no cash repayment) |

The cost-speed trade-off — faster access to capital almost always means higher cost

How to Choose the Right Debt

The decision framework for choosing debt is driven by three factors:

Factor 1: Purpose

What are you using the money for? Match the type of debt to the purpose.

| Purpose | Best Debt Type | Why |

|---|---|---|

| Smoothing cash flow between invoice and payment | Invoice financing or overdraft | Short-term need, repaid from incoming cash |

| Purchasing a specific asset | Asset finance or term loan | The asset serves as security, reducing cost |

| Funding growth (marketing, hiring) | Revenue-based financing or term loan | Repayment is tied to the revenue the growth generates |

| Bridging to the next equity round | Convertible note | Avoids setting a valuation during a transition period |

| General working capital | Overdraft or term loan | Flexible, multi-purpose |

Factor 2: Cost

What is the total cost of the debt, including all fees, interest, and hidden charges? Always calculate the effective annual rate, not just the headline rate. A merchant cash advance that charges a 1.3x factor on a 6-month advance has an effective annual rate of over 60% — far more expensive than it appears.

Factor 3: Covenants and Conditions

What are you agreeing to beyond the repayment? Debt covenants are conditions that the lender imposes on your business — minimum revenue levels, maximum debt ratios, restrictions on additional borrowing, and reporting requirements. Breaching a covenant can trigger immediate repayment of the entire loan, even if you have never missed a payment.

| Covenant | What It Requires | Why Lenders Impose It |

|---|---|---|

| Debt Service Coverage Ratio (DSCR) | Your operating income must be at least 1.2-1.5x your debt payments | Ensures you can afford the repayments |

| Loan-to-Value (LTV) | The loan must not exceed a certain % of the asset's value | Protects the lender if they need to seize and sell the asset |

| Minimum cash balance | You must maintain a minimum amount of cash in the bank | Ensures you have a buffer for unexpected expenses |

| No additional borrowing | You cannot take on more debt without the lender's permission | Prevents you from over-leveraging the business |

| Regular reporting | You must provide monthly or quarterly financial statements | Allows the lender to monitor the business's health |

The Golden Rules of Debt

Rule 1: Never borrow to survive.

Debt should fund growth, not cover losses. If your business is losing money and you borrow to keep the lights on, you are not solving the problem — you are making it worse. Fix the business model first, then borrow to scale it.

Rule 2: Always know your debt service capacity.

Before borrowing, calculate exactly how much debt your business can service from its current cash flow. The formula is simple: Maximum Monthly Debt Payment = (Monthly Operating Cash Flow) × 0.5. Never commit more than 50% of your operating cash flow to debt service. The remaining 50% is your buffer for unexpected expenses, seasonal fluctuations, and growth investment.

Rule 3: Read every word of the agreement.

Every word. Every clause. Every schedule. If you do not understand something, ask your lawyer to explain it. If your lawyer cannot explain it in plain English, get a different lawyer.

Rule 4: Personal guarantees are a last resort.

Many lenders will ask for a personal guarantee — a commitment that you will personally repay the debt if the business cannot. This means your house, your savings, and your personal assets are at risk. Only agree to a personal guarantee if you have exhausted all other options and you are confident in the business's ability to repay.

Rule 5: Build relationships with lenders before you need them.

The worst time to approach a bank is when you desperately need money. The best time is when you do not need it at all. Open a business account early. Meet your relationship manager. Share your financials proactively. When you eventually need to borrow, you will be a known quantity, not a cold application.

Checklist — Complete Before Moving On

What is the specific purpose of the borrowing?

What type of debt is most appropriate for this purpose?

What is the effective annual cost (including all fees)?

Can the business service this debt from current cash flow (within the 50% rule)?

What covenants are attached, and can you meet them?

Is a personal guarantee required? If so, what is the maximum exposure?

What happens if the business cannot repay? What are the consequences?

Have you had the agreement reviewed by a lawyer?

Always use the cheapest appropriate capital first.

ANGEL & SEED

"The first external equity — and the most important relationship you will ever form."

What This Layer Is About

Angel and seed investment is the moment your business stops being entirely yours and starts being partly someone else's. This is a profound transition, and it should not be entered into lightly. When you take equity investment, you are not just accepting money — you are accepting a partner. A partner who will have opinions about how you run the business, who will expect regular updates and financial transparency, and who will have legal rights that constrain your freedom of action.

Done well, angel and seed investment is transformative. The right investor brings not just capital but expertise, connections, credibility, and accountability. Done poorly, it is a trap — the wrong investor at the wrong valuation on the wrong terms can cripple a business more effectively than any competitor.

Understanding Angel Investors

An angel investor is an individual who invests their own money in early-stage businesses, typically in exchange for equity. Angels are the most common source of first external capital for startups, and they operate very differently from institutional investors.

What Angels Look For

| Factor | What They Want | How to Demonstrate It |

|---|---|---|

| The Founder | Someone they believe in — passionate, resilient, coachable, and honest | Your personal story, your track record, your energy in the meeting |

| The Market | A large, growing market with a clear problem that needs solving | Bottom-up market sizing with credible sources |

| The Traction | Evidence that the business is working — revenue, users, partnerships, waitlists | Specific metrics, not vanity metrics |

| The Return Potential | A realistic path to a 10-20x return on their investment within 5-7 years | A credible vision, comparable exits, and a clear growth trajectory |

| The Terms | A fair valuation and standard terms that protect their investment without being predatory | Alignment with market norms for your stage and sector |

What Angels Bring Beyond Money

| Value-Add | How It Helps | How to Assess It |

|---|---|---|

| Industry expertise | Guidance on strategy, product, and market positioning | Ask about their operating experience in your sector |

| Network access | Introductions to customers, partners, and future investors | Ask for specific examples of introductions they have made for other portfolio companies |

| Credibility | Their name on your cap table signals quality to future investors | Research their reputation and portfolio |

| Mentorship | Regular coaching and accountability | Ask how often they meet with their portfolio companies |

| Follow-on capital | Ability to invest in future rounds | Ask about their typical follow-on investment strategy |

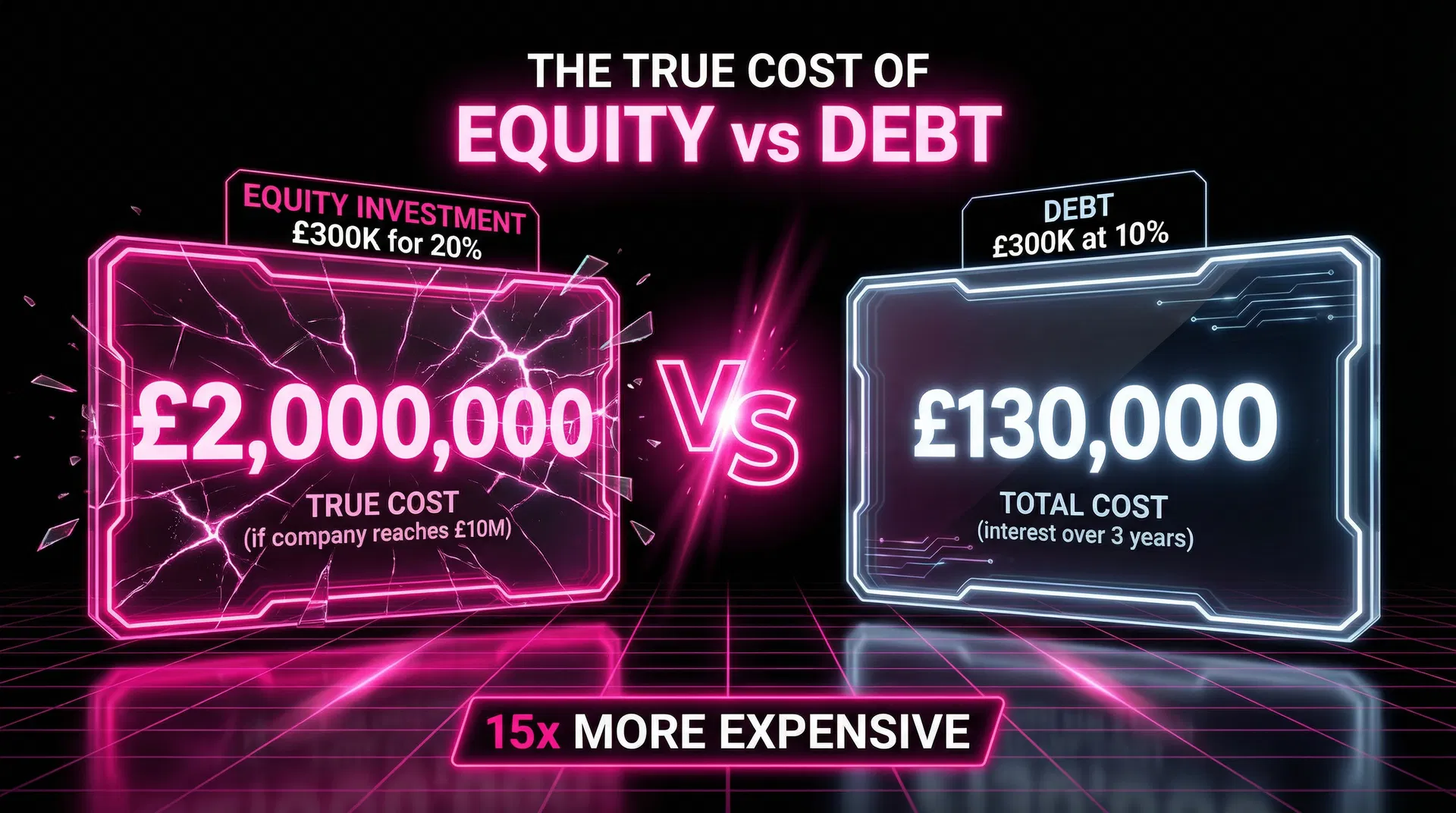

Equity is the most expensive capital — understand the true cost before you give up ownership

Understanding Seed Funds

Seed funds are small venture capital funds (typically £5-50M in size) that specialise in early-stage investments. They write larger cheques than individual angels (£100K-£1M) and operate with more structure — investment committees, due diligence processes, and formal governance.

| Dimension | Angel Investor | Seed Fund |

|---|---|---|

| Decision-making | Individual decision, often fast (days to weeks) | Committee decision, slower (weeks to months) |

| Cheque size | £10,000-£100,000 | £100,000-£1,000,000 |

| Due diligence | Light — often based on personal assessment | Formal — financial, legal, and commercial review |

| Board involvement | Advisory, informal | Often takes a board seat with formal governance |

| Follow-on | Variable — depends on personal capacity | Usually reserves capital for follow-on rounds |

| Portfolio size | 5-20 investments | 20-50+ investments |

| Value-add | Personal — based on individual experience | Institutional — access to fund's network, resources, and platform |

Structuring the Angel/Seed Round

The structure of your first equity round sets the template for every round that follows. Get it right, and you create a clean, investor-friendly cap table that makes future fundraising easier. Get it wrong, and you create a mess that will haunt you for years.

Priced Round vs Convertible Instrument

| Structure | How It Works | When to Use It |

|---|---|---|

| Priced round (equity) | Investors buy shares at a fixed price, based on an agreed valuation | When you have enough traction to justify a valuation and enough investor interest to fill the round |

| Convertible note | Investors lend money that converts to equity at the next priced round, usually at a discount | When you need capital quickly and do not want to set a valuation yet |

| SAFE | Similar to a convertible note but without interest or a maturity date | When you want the simplicity of a convertible instrument without the debt characteristics |

| ASA | The UK equivalent of a SAFE, structured as a forward subscription for shares | The standard convertible instrument for UK companies |

Valuation

At the angel/seed stage, valuation is more art than science. There is no formula that will give you a "correct" valuation. Instead, valuation is determined by a combination of:

| Factor | Impact on Valuation |

|---|---|

| Revenue and growth rate | Higher revenue and faster growth = higher valuation |

| Market size | Larger addressable market = higher valuation |

| Team quality | Stronger team with relevant experience = higher valuation |

| Competitive landscape | Less competition or stronger differentiation = higher valuation |

| Comparable transactions | What similar companies raised at similar stages |

| Investor demand | More investors competing to invest = higher valuation |

Typical Seed Valuations (UK, 2024-2026)

| Stage | Typical Pre-Money Valuation | Typical Round Size |

|---|---|---|

| Pre-revenue, strong team and concept | £500K-£2M | £100K-£500K |

| Early revenue (£5-15K MRR) | £2M-£5M | £300K-£1M |

| Growing revenue (£15-50K MRR) | £4M-£10M | £500K-£2M |

| Strong revenue (£50K+ MRR) | £8M-£20M | £1M-£5M |

The Option Pool

Before closing the round, you will need to create an employee stock option pool (ESOP) — a reserve of shares set aside for future hires. The standard size is 10-15% of the post-money capitalisation. This pool is typically created before the investment, which means the dilution comes from the founders, not the investors. Negotiate the pool size carefully — a larger pool means more dilution for you.

SEIS and EIS Tax Relief

The UK's Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS) are among the most generous tax incentives for startup investment in the world. They provide significant tax relief to investors, which makes your company dramatically more attractive to UK angel investors.

| Scheme | Tax Relief for Investor | Maximum Investment | Company Eligibility |

|---|---|---|---|

| SEIS | 50% income tax relief + CGT exemption on gains + loss relief | £200,000 per investor per year | Under 3 years old, fewer than 25 employees, assets under £350K |

| EIS | 30% income tax relief + CGT deferral + loss relief | £1M per investor per year (£2M for knowledge-intensive companies) | Under 7 years old (or 10 for KICs), fewer than 250 employees, assets under £15M |

Why This Matters: An investor who puts £100,000 into an SEIS-qualifying company effectively risks only £50,000 (after the 50% tax relief). If the investment fails completely, loss relief reduces the effective loss further. This dramatically lowers the barrier for angel investors and is one of the strongest selling points for UK startups. Ensure your company has advance assurance from HMRC before approaching investors.

Checklist — Complete Before Moving On

Have you exhausted bootstrapping and non-dilutive options first?

Do you have enough traction to justify external investment?

Have you decided between a priced round and a convertible instrument?

Do you have a realistic valuation range based on comparables?

Have you obtained SEIS/EIS advance assurance from HMRC?

Have you created an option pool of appropriate size (10-15%)?

Have you identified 30-50 potential angel investors and seed funds?

Do you understand the terms you are willing to accept and the terms you will reject?

Have you engaged a lawyer experienced in startup fundraising?

Are you prepared for the time commitment (3-6 months of active fundraising)?

The right investor is worth more than the right valuation.

INSTITUTIONAL

"Venture capital, private equity, and the big leagues."

What This Layer Is About

Institutional capital is the top of the stack. It is the largest cheques, the most demanding investors, and the highest stakes. Venture capital firms, private equity funds, and strategic corporate investors operate at a scale and with a level of sophistication that is fundamentally different from angel investors and seed funds. They deploy millions — often tens of millions — in a single transaction, and they expect a level of governance, reporting, and performance that will transform how you run your business.

This layer is not for every business. In fact, it is not for most businesses. Institutional capital is designed for companies that are pursuing rapid, exponential growth in large markets — companies that have the potential to become worth hundreds of millions or billions. If your ambition is to build a profitable, sustainable business doing £5M in revenue, institutional capital is not the right tool. It will impose expectations and pressures that are misaligned with your goals. But if your ambition is to build a market leader — to dominate a category, to scale internationally, to create something that changes an industry — then institutional capital is the fuel that makes it possible. And understanding how it works is essential.

Venture Capital: How It Actually Works

Most founders misunderstand venture capital because they see it from the outside — the press releases, the headline valuations, the success stories. From the inside, VC is a very specific business with very specific economics, and understanding those economics is the key to understanding how VCs make decisions.

The VC Economics

| Component | Detail |

|---|---|

| Fund size | Typically £20M-£500M+ |

| Management fee | 2% of fund size per year, paid to the VC firm to cover salaries and operating costs |

| Carried interest ("carry") | 20% of profits above a hurdle rate (typically 8%), paid to the VC partners as their performance bonus |

| Investment period | Years 1-5: actively investing in new companies |

| Harvest period | Years 5-10: managing existing investments and seeking exits |

| Target return | 3x net return to LPs (i.e., a £100M fund must return £300M) |

They need big outcomes. A £100M fund that needs to return £300M cannot achieve this through modest exits. It needs at least 2-3 investments that return 10-50x. This is why VCs are only interested in businesses with the potential to become very large. A business that will reliably grow to £10M in revenue is not interesting to a VC — even if it is a great business — because a £10M revenue business will not generate the 10-50x return they need.

They expect most investments to fail. The typical VC portfolio follows a power law distribution: 1-2 investments generate the vast majority of returns, a few break even, and the rest lose money. VCs accept this because the winners more than compensate for the losers. But it means that every investment decision is made through the lens of "could this be one of the 1-2 winners?"

They have a fixed timeline. The fund must return capital within 10 years. This means VCs need an exit — an IPO, an acquisition, or a secondary sale — within that timeframe. If your business is not on a trajectory to exit within 5-7 years of their investment, they will not invest.

What Institutional Investors Evaluate

| Dimension | What They Want to See | How They Assess It |

|---|---|---|

| Market | A large, growing market (£1B+ TAM) with structural tailwinds | Market research, industry reports, expert calls |

| Product-market fit | Strong evidence that customers love the product and are willing to pay | Net Promoter Score, retention cohorts, organic growth metrics |

| Unit economics | Proven, positive unit economics with a clear path to improvement at scale | CAC, LTV, gross margin, payback period — all with 12+ months of data |

| Growth rate | Rapid, consistent growth — typically 2-3x year-over-year | Monthly revenue data, growth rate trends, leading indicators |

| Team | A world-class team with relevant experience and the ability to scale | Track records, references, organisational design |

| Moat | A defensible competitive advantage that compounds over time | Network effects, switching costs, proprietary data, brand |

| Capital efficiency | Evidence that the business can generate significant returns per pound invested | Revenue per employee, burn multiple, magic number |

The Burn Multiple

One metric that institutional investors increasingly focus on is the burn multiple — the ratio of net cash burned to net new ARR generated. It measures how efficiently you are converting capital into growth.

| Burn Multiple | Rating | What It Means |

|---|---|---|

| Below 1x | Amazing | You are generating more new ARR than you are burning — highly capital-efficient |

| 1-1.5x | Great | Efficient growth — investors will be very interested |

| 1.5-2x | Good | Acceptable for early-stage companies with strong growth rates |

| 2-3x | Mediocre | Investors will question your efficiency and want a clear path to improvement |

| Above 3x | Concerning | You are burning too much relative to growth — fix this before raising |

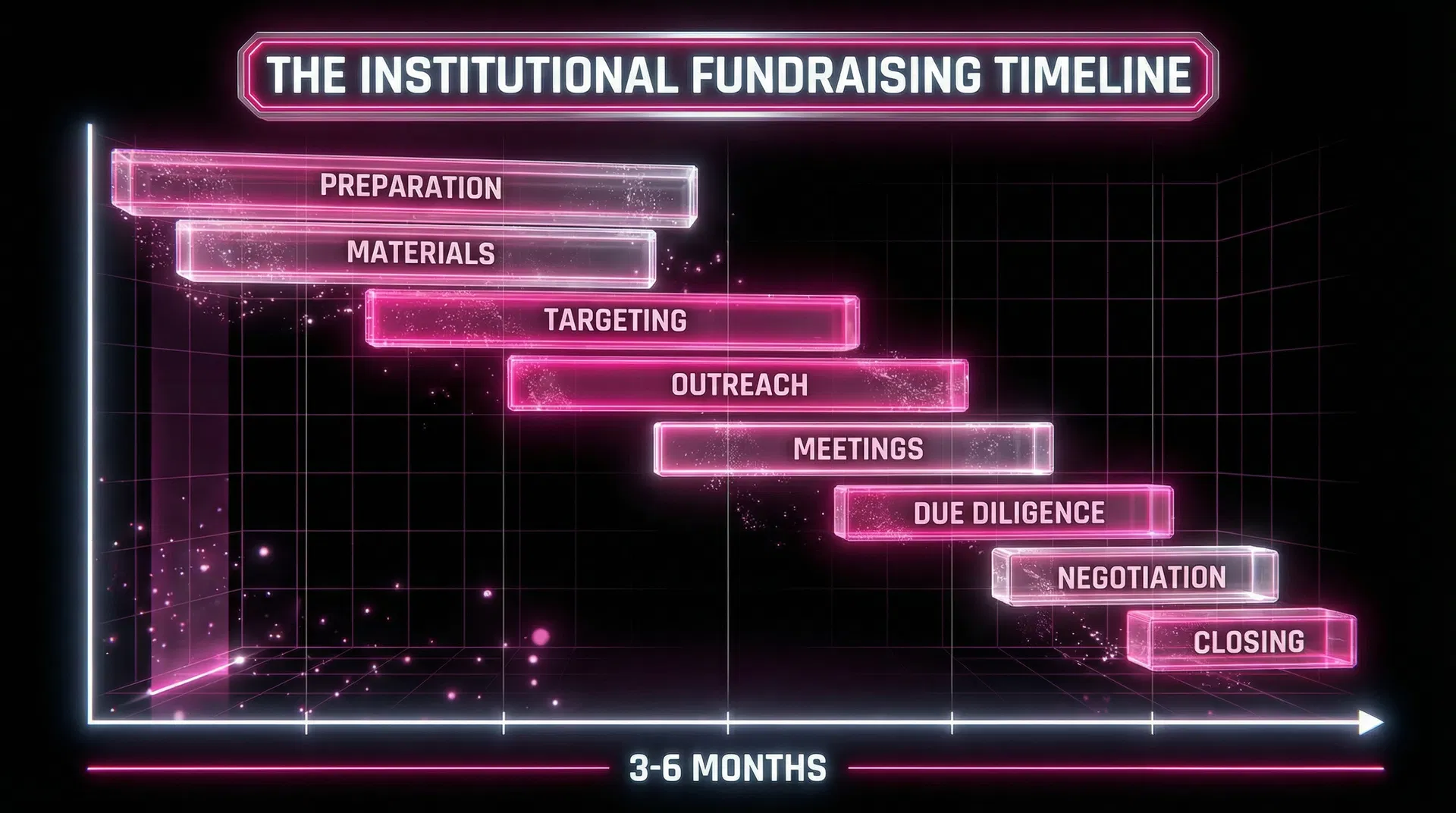

The Institutional Fundraising Process

Raising institutional capital is a structured, multi-stage process that typically takes 3-6 months from first meeting to money in the bank.

| Stage | Duration | What Happens |

|---|---|---|

| 1. Preparation | 4-8 weeks | Build the data room, refine the pitch deck, prepare the financial model, identify target funds |

| 2. Outreach | 2-4 weeks | Secure introductions, send materials, schedule meetings |

| 3. First meetings | 2-4 weeks | 30-60 minute meetings with partners at target funds |

| 4. Partner meetings | 2-4 weeks | Deeper sessions with the full partnership, often including product demos and customer references |

| 5. Due diligence | 4-8 weeks | Financial, legal, commercial, and technical due diligence by the fund's team and external advisors |

| 6. Term sheet | 1-2 weeks | Negotiation of key terms |

| 7. Legal documentation | 4-6 weeks | Drafting and negotiation of final legal agreements |

| 8. Closing | 1-2 weeks | Signing, funding, and board formation |

Expect 3-6 months from first meeting to money in the bank — plan your runway accordingly

The Data Room

At the institutional level, the data room must be comprehensive, organised, and current. Investors will judge your operational competence by the quality of your data room.

| Section | Documents |

|---|---|

| Corporate | Articles of association, shareholder agreements, board minutes, cap table, option pool details |

| Financial | Audited accounts (if available), management accounts (monthly, last 24 months), financial model with assumptions, bank statements |

| Commercial | Customer list, key contracts, pipeline data, churn analysis, NPS data |

| Product | Product roadmap, technical architecture, IP documentation, security audits |

| Team | Org chart, key employment contracts, compensation benchmarks, hiring plan |

| Legal | Any litigation, regulatory filings, compliance certificates, material contracts |

| Market | Market sizing analysis, competitive landscape, industry reports |

Negotiating Institutional Terms

The terms at the institutional level are more complex and more consequential than at the angel/seed stage. Institutional investors will typically require "protective provisions" — a list of actions that the company cannot take without the investor's consent.

| Action | Why Investors Want Approval Rights |

|---|---|

| Issuing new shares | Prevents dilution without their knowledge |

| Taking on significant debt | Prevents over-leveraging the business |

| Selling the company | Ensures they have a say in exit decisions |

| Changing the company's business | Prevents a pivot that undermines their investment thesis |

| Hiring/firing the CEO | Ensures leadership stability |

| Declaring dividends | Prevents cash being extracted before they achieve a return |

| Changing the articles of association | Prevents changes to their rights |

These provisions are standard and generally reasonable. The negotiation is about the thresholds — how much debt triggers approval? What constitutes a "significant" change to the business? Push for thresholds that give you operational freedom for day-to-day decisions while giving investors appropriate oversight on major strategic decisions.

When to Pursue Institutional Capital

Not every business should raise institutional capital. Here is the decision framework:

| Signal | Pursue Institutional Capital | Do Not Pursue |

|---|---|---|

| Market size | £1B+ addressable market | Niche market with limited scale potential |

| Growth rate | 2-3x year-over-year or faster | Steady, linear growth |

| Unit economics | Proven and positive, with clear path to improvement | Unproven or negative with no clear fix |

| Competitive dynamics | Winner-take-most market where speed matters | Fragmented market where speed is less important |

| Founder ambition | Build a category-defining company | Build a profitable, sustainable lifestyle business |

| Capital requirements | Significant capital needed to capture the opportunity | Growth can be funded from revenue |

Checklist — Complete Before Moving On

Is your market large enough (£1B+ TAM) to justify institutional investment?

Are you growing at 2x+ year-over-year?

Are your unit economics proven and positive?

Do you have 12+ months of financial data to share?

Is your data room complete, organised, and current?

Have you identified 20-30 target funds that invest in your stage and sector?

Do you have warm introductions to at least 10 of them?

Have you engaged experienced legal counsel for the negotiation?

Do you understand the implications of every term you are being asked to accept?

Are you prepared for the governance, reporting, and accountability that comes with institutional capital?

Institutional capital is not for every business. In fact, it is not for most businesses.

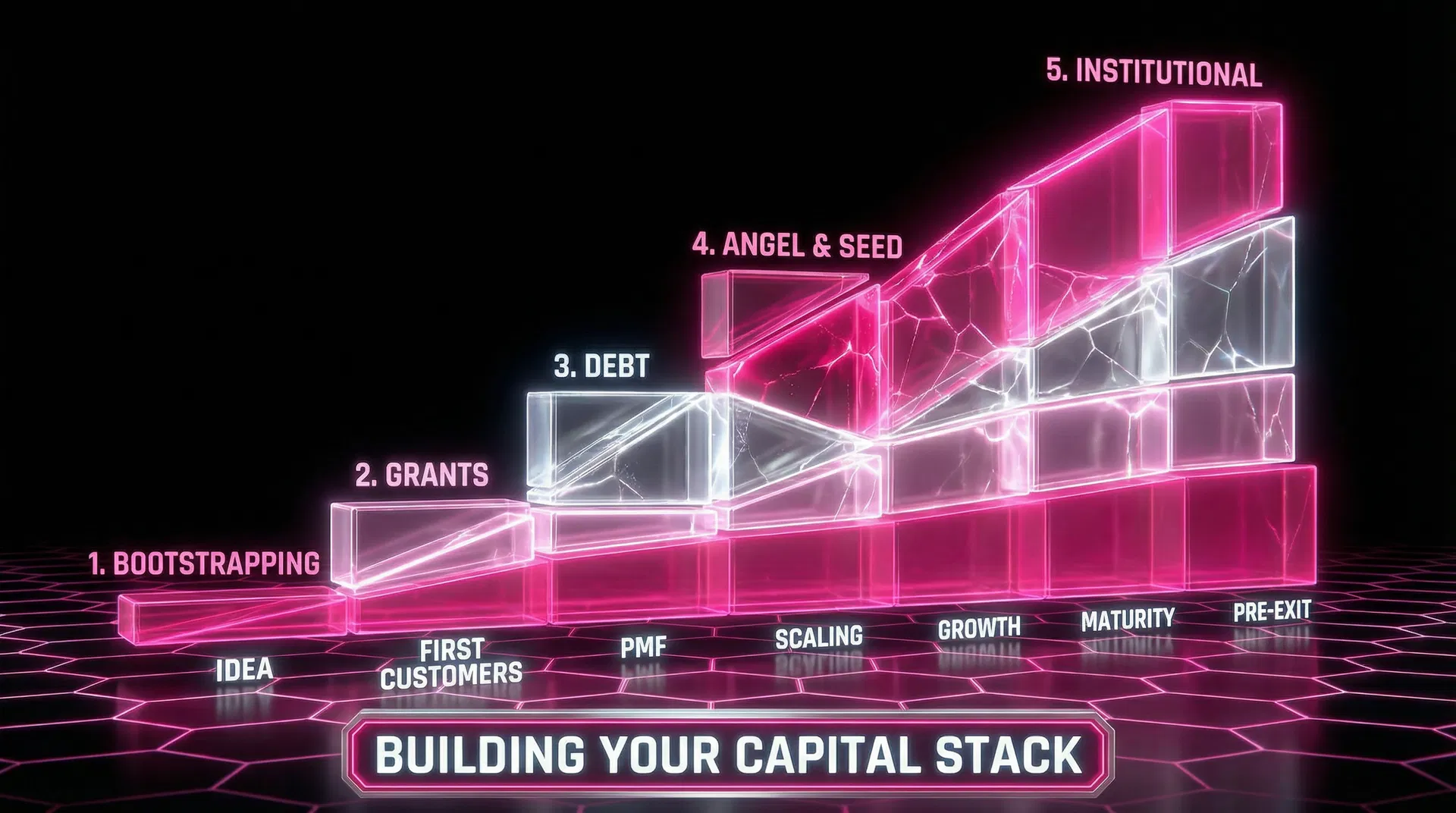

Putting It All Together: Building Your Capital Stack

The most successful businesses do not rely on a single source of capital. They build a stack — layering different types of funding on top of each other, each serving a specific purpose at a specific stage.

The Ideal Capital Stack Progression

| Stage | Business Milestone | Capital Layer | Purpose |

|---|---|---|---|

| Idea / Pre-revenue | Validating the concept | Bootstrapping | Prove the idea works without giving anything away |

| First customers | £1-10K MRR | Bootstrapping + Grants | Extend runway with non-dilutive capital |

| Product-market fit | £10-50K MRR | Angel / Seed | First equity capital to accelerate growth |

| Scaling | £50-200K MRR | Seed / Series A + Debt | Equity for growth investment, debt for working capital |

| Growth | £200K+ MRR | Institutional (Series A/B) | Significant capital for market expansion and team scaling |

| Maturity | Profitable or near-profitable | Debt + Revenue-based financing | Non-dilutive capital for continued growth |

| Pre-exit | Preparing for IPO or acquisition | Mezzanine / Growth equity | Final capital to maximise valuation before exit |

The complete capital stack journey — each layer builds on the one below it

Always use the cheapest appropriate capital first. Bootstrapping before grants. Grants before debt. Debt before equity. Equity from angels before equity from institutions. Every layer of the stack has a cost, and using the most expensive capital when cheaper alternatives are available is a strategic error.

The Capital Stack Manifesto

THE CAPITAL STACK

MANIFESTO

Save this. Print it. Pin it above your desk.

Capital is a tool, not a trophy.

Raising money is not an achievement. Building a profitable, sustainable business is an achievement. Capital is the tool that helps you get there — nothing more.

The cheapest capital is always the best capital.

Revenue is cheaper than grants. Grants are cheaper than debt. Debt is cheaper than equity. Always exhaust the cheaper options before moving to the more expensive ones.

Every pound of equity you give away is a pound you never get back.

Dilution is permanent. Be strategic about when, how much, and to whom you sell equity. Every percentage point matters.

The right investor is worth more than the right valuation.

An investor who brings expertise, connections, and genuine support at a slightly lower valuation is almost always a better deal than a passive investor at a higher valuation.

Understand every term before you sign.

If you do not understand a clause, do not sign it. If your lawyer cannot explain it in plain English, get a different lawyer.

Build relationships before you need capital.

The worst time to meet an investor is when you are desperate for money. The best time is when you do not need it. Start building relationships 12-18 months before you plan to raise.

Cash flow is the ultimate capital.

The business that generates its own cash flow is the business that has the most options, the most leverage, and the most freedom. Everything else is a bridge to get there.

This Framework Is the Map.

Capital Catalyst Is the Compass.

This framework has given you the complete map of the capital landscape. But navigating that landscape — choosing the right capital at the right time, negotiating the right terms, and building the relationships that make it all possible — requires guidance from someone who has been on every side of the table. The Capital Catalyst course walks you through the entire Capital Stack System with video tutorials, downloadable templates, live case studies, and direct access to me and my team.

Copyright Matt Haycox. All rights reserved. The Capital Stack System™ is a trademark of Matt Haycox.